Printable PDF

Printable PDFTest Prep CPA-REGULATION Exam Preparation Materials

Vendor: Test Prep

Exam Code: CPA-REGULATION

Exam Name: CPA Regulation

Certification: Test Prep Certifications

Total Questions: 69 Q&A

( View

Details)

Updated on: Jul 09, 2026

Note: Product instant download. Please sign in and click My account to download your product.

How Our Test Prep CPA-REGULATION Preparation Approach Works

Preparing for the Test Prep CPA-REGULATION Test Prep Certifications certification exam requires more than repetitive practice — it requires a clear preparation structure aligned with real exam objectives, question patterns, and learning efficiency.

At Leads4pass, our approach focuses on aligning preparation materials with current exam objectives, question patterns, and learning efficiency. Instead of overwhelming candidates with unfocused content, we organize practice around what truly matters in the Test Prep CPA-REGULATION exam, helping candidates build stable understanding and confident answering strategies.

Through structured practice, exam-style simulations, and clear explanations, candidates are guided to prepare with purpose, reduce uncertainty, and approach the Test Prep Certifications exam with confidence.

How We Structure Test Prep CPA-REGULATION Exam Preparation

Our preparation materials are not assembled randomly. They are structured around a clear methodology:

- Breaking down official exam objectives into focused learning modules

- Prioritizing high-impact and commonly misunderstood topics

- Using practice questions to validate understanding, not memorization

- Maintaining consistency between preparation and real exam expectations

This structure allows candidates to study efficiently while maintaining clarity and direction throughout the preparation process.

Maintaining Relevance Without Disrupting Learning Flow

To keep preparation aligned with current exam expectations, Test Prep CPA-REGULATION materials are maintained through a regular review and update cycle, ensuring alignment with evolving exam objectives while preserving a consistent learning experience.

Candidates can switch between PDF-based review and VCE-style practice depending on their study rhythm, allowing flexibility without unnecessary distractions. Throughout the process, learning remains focused, private, and uninterrupted.

How Candidates Typically Use This Page

- Candidates new to networking often begin with structured review and gradually move into exam-style practice

- Experienced professionals typically focus on targeted practice to refine weaker areas

- Candidates retaking the exam use focused simulations to rebuild confidence and answering consistency

Rather than enforcing a single study path, the materials adapt to the candidate’s experience level and preparation goals.

Avoiding Common Test Prep Certifications Preparation Pitfalls

- Practicing without understanding underlying concepts

- Studying outdated or misaligned content

- Preparing without exposure to real exam-style scenarios

- Lacking a structured review strategy

Our preparation framework is designed specifically to avoid these pitfalls and support efficient, focused learning.

What You Gain from Test Prep CPA-REGULATION Preparation

- A structured preparation framework aligned with exam objectives

- Practice that reinforces understanding, not memorization

- Flexible study formats that adapt to individual learning styles

- A focused, distraction-free preparation experience

- Greater clarity and confidence approaching exam day

If your goal is to prepare for the Test Prep Certifications exam with clarity and efficiency, you can begin a structured preparation process designed around real exam expectations.

- 99.5% pass rate

- 12 Years experience

- 7000+ IT Exam Q&As

- 70000+ satisfied customers

- 365 days Free Update

- 3 days of preparation before your test

- 100% Safe shopping experience

- 24/7 Support

Test Prep CPA-REGULATION Last Month Results

Free CPA-REGULATION Exam Questions in PDF Format

- File

- Size

- Test Prep_leads4pass_CPA-REGULATION_by_soufiane_67.pdf

- 215.77 KB

- Test Prep_leads4pass_CPA-REGULATION_by_nagesha_59.pdf

- 248.13 KB

- Test Prep_leads4pass_CPA-REGULATION_by_Timothy_Brown_65.pdf

- 244.09 KB

- Test Prep_leads4pass_CPA-REGULATION_by_Bungle_57.pdf

- 234.61 KB

- Test Prep_leads4pass_CPA-REGULATION_by_n-adiw_64.pdf

- 227.61 KB

- Test Prep_leads4pass_CPA-REGULATION_by_dunmarish_65.pdf

- 227.69 KB

CPA-REGULATION Online Practice Questions and Answers

Under a $150,000 insurance policy on her deceased father's life, May Green is to receive $12,000 per year for 15 years. Of the $12,000 received in 1987, the amount subject to income tax is:

A. $0

B. $1,000

C. $2,000

D. $12,000

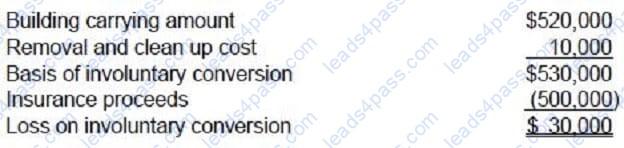

On December 31, 1989, a building owned by Pine Corp. was totally destroyed by fire. The building had fire insurance coverage up to $500,000. Other pertinent information as of December 31, 1989 follows:

During January 1990, before the 1989 financial statements were issued, Pine received insurance proceeds of $500,000. On what amount should Pine base the determination of its loss on involuntary conversion?

A. $520,000

B. $530,000

C. $550,000

D. $560,000

Hall, a divorced person and custodian of her 12-year old child, filed her 1990 federal income tax return as head of a household. She submitted the following information to the CPA who prepared her 1990 return:

• In 1990, Hall sold an antique that she bought in 1980 to display in her home. Hall paid $800 for the antique and sold it for $1,400, using the proceeds to pay a court ordered judgment.

The $600 gain that Hall realized on the sale of the antique should be treated as:

A. Ordinary income.

B. Long-term capital gain.

C. An involuntary conversion.

D. A nontaxable antiquities transaction.

Hot Exams

Leads4Pass Test Prep Certifications CPA-REGULATION Exam Solutions

The following table comprehensively analyzes the quality and value of Test Prep Certifications CPA-REGULATION exam materials.

100% safe shopping

100% real and effective

100% money back guarantee

Leads4Pass guarantee comes from more than 10 years of experience and reputation

![]()

![]()

![]()

![]()

![]()

![]()

All rights are reserved by

leads4pass.com. Any changes, copy or trademarks abuse will be

regarded as infringement.

leads4pass.com will reserve the right to pursue accountability.

Copyright © 2004-

2026 leads4pass.com.