FINANCIAL-ACCOUNTING-AND-REPORTING Online Practice Questions and Answers

Which of the following statements best describes an operating procedure for issuing a new Financial Accounting Standards Board (FASB) statement?

A. The emerging issues task force must approve a discussion memorandum before it is disseminated to the public.

B. The exposure draft is modified per public opinion before issuing the discussion memorandum.

C. A new statement is issued only after a majority vote by the members of the FASB.

D. A new FASB statement can be rescinded by a majority vote of the AICPA membership.

Income tax-basis financial statements differ from those prepared under GAAP in that income tax-basis financial statements:

A. Do not include nontaxable revenues and nondeductible expenses in determining income.

B. Include detailed information about current and deferred income tax liabilities.

C. Contain no disclosures about capital and operating lease transactions.

D. Recognize certain revenues and expenses in different reporting periods.

An extraordinary gain should be reported as a direct increase to which of the following?

A. Net income.

B. Comprehensive income.

C. Income from continuing operations, net of tax.

D. Income from discontinued operations, net of tax.

Foy Corp. failed to accrue warranty costs of $50,000 in its December 31, 1992, financial statements. In addition, a $30,000 change from straight-line to accelerated depreciation was made at the beginning of 1993. Both the $50,000 and the $30,000 are net of related income taxes. What amount should Foy report as prior period adjustments in 1993?

A. $0

B. $30,000

C. $50,000

D. $80,000

In 1992, hail damaged several of Toncan Co.'s vans. Hailstorms had frequently inflicted similar damage to Toncan's vans. Over the years, Toncan had saved money by not buying hail insurance and either paying for repairs, or selling damaged vans and then replacing them. In 1992, the damaged vans were sold for less than their carrying amount. How should the hail damage cost be reported in Toncan's 1992 financial statements?

A. The actual 1992 hail damage loss as an extraordinary loss, net of income taxes.

B. The actual 1992 hail damage loss in continuing operations, with no separate disclosure.

C. The expected average hail damage loss in continuing operations, with no separate disclosure.

D. The expected average hail damage loss in continuing operations, with separate disclosure.

Which of the following should be disclosed in a summary of significant accounting policies?

A. Basis of profit recognition on long-term construction contracts.

B. Future minimum lease payments in the aggregate and for each of the five succeeding fiscal years.

C. Depreciation expense.

D. Composition of sales by segment.

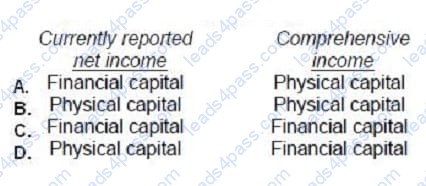

FASB's conceptual framework explains both financial and physical capital maintenance concepts. Which capital maintenance concept is applied to currently reported net income, and which is applied to comprehensive income?

A. Option A

B. Option B

C. Option C

D. Option D

Coffey Corp.'s trial balance of Income Statement Accounts for the year ended December 31, 1988 as follows:

Coffey's income tax rate is 30%. The gain on debt extinguishment is considered a usual and recurring part of Coffey's operations. The hurricane is considered an unusual and infrequent event. Coffey prepares a multiple-step income statement for 1988.

Net income is:

A. $140,000

B. $161,000

C. $168,000

D. $200,000

Gown, Inc. sold a warehouse and used the proceeds to acquire a new warehouse. The excess of the proceeds over the carrying amount of the warehouse sold should be reported as a(an):

A. Extraordinary gain, net of income taxes.

B. Part of continuing operations.

C. Gain from discontinued operations, net of income taxes.

D. Reduction of the cost of the new warehouse.

During 1990, Fuqua Steel Co. had the following unusual financial events occur:

•

Bonds payable were retired five years before their scheduled maturity, resulting in a $260,000 gain. Fuqua has frequently retired bonds early when interest rates declined significantly.

•

A steel forming segment suffered $255,000 in losses due to hurricane damage. This was the fourth similar loss sustained in a 5-year period at that location.

•

A component of Fuqua's operations, steel transportation, was sold at a net loss of $350,000.

This was Fuqua's first divestiture of one of its operating segments.

Before income taxes, what amount should be disclosed as the gain (loss) from extraordinary items in

1990?

A. $0

B. $5,000

C. $(90,000)

D. $(350,000)

![]()

![]()

![]()

![]()

![]()

![]()

All rights are reserved by

leads4pass.com. Any changes, copy or trademarks abuse will be

regarded as infringement.

leads4pass.com will reserve the right to pursue accountability.

Copyright © 2004-

2026 leads4pass.com.