CPA-TEST Online Practice Questions and Answers

An auditor is reporting on condensed financial statements for an annual period that are derived from the audited financial statements of a publicly-held entity. The auditor's opinion should indicate whether the information in the condensed financial statements is fairly stated in all material respects:

A. In conformity with accounting principles generally accepted in the United States of America.

B. In relation to the complete financial statements.

C. In conformity with another comprehensive basis of accounting.

D. In relation to supplementary filings under federal security statutes.

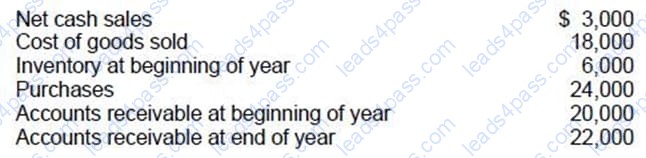

Selected data pertaining to ABC Co. for the calendar year 20X4 is as follows: What was the inventory turnover for 20X4?

A. 1.2 times.

B. 1.5 times.

C. 2.0 times.

D. 3.0 times.

The purpose of segregating the duties of hiring personnel and distributing payroll checks is to separate the:

A. Human resources function from the controllership function.

B. Administrative controls from the internal accounting controls.

C. Authorization of transactions from the custody of related assets.

D. Operational responsibility from the recordkeeping responsibility.

Property acquisitions that are misclassified as maintenance expense would most likely be detected by an internal accounting control system that provides for:

A. Investigation of variances within a formal budgeting system.

B. Review and approval of the monthly depreciation entry by the plant supervisor.

C. Segregation of duties of employees in the accounts payable department.

D. Examination by the internal auditor of vendor invoices and canceled checks for property acquisitions.

Which of the following is an engagement attribute for an audit of an entity that processes most of its financial data in electronic form without any paper documentation?

A. Discrete phases of planning, interim, and year-end fieldwork.

B. Increased effort to search for evidence of management fraud.

C. Performance of audit tests on a continuous basis.

D. Increased emphasis on the completeness assertion.

When an auditor tests the internal controls of a computerized accounting system, which of the following is true of the test data approach?

A. Test data are coded to a dummy subsidiary so they can be extracted from the system under actual operating conditions.

B. Test data programs need not be tailor-made by the auditor for each client's computer applications.

C. Test data programs usually consist of all possible valid and invalid conditions regarding compliance with internal controls.

D. Test data are processed with the client's computer and the results are compared with the auditor's predetermined results.

Which of the following statements most likely represents a disadvantage for an entity that keeps microcomputer-prepared data files rather than manually prepared files?

A. It is usually more difficult to detect transposition errors.

B. Transactions are usually authorized before they are executed and recorded.

C. It is usually easier for unauthorized persons to access and alter the files.

D. Random error associated with processing similar transactions in different ways is usually greater.

Under the Revised Model Business Corporation Act, following what type of corporate acquisition does the acquiring corporation automatically become liable for all obligations of the acquired corporation?

A. A leveraged buyout of assets.

B. An acquisition of stock for debt securities.

C. A cash tender offer.

D. A merger.

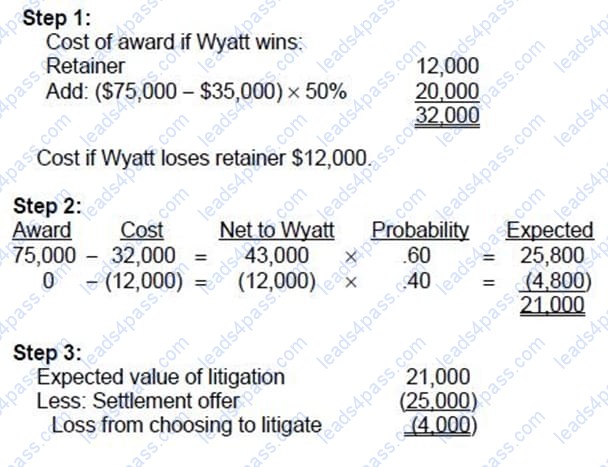

A vendor offered ABC Co. $25,000 compensation for losses resulting from faulty raw materials.

Alternately, a lawyer offered to represent ABC in a lawsuit against the vendor for a $12,000 retainer and 50% of any award over $35,000. Possible court awards with their associated probabilities are:

Compared to accepting the vendor's offer, the expected value for ABC to litigate the matter to verdict provides a:

A. $4,000 loss.

B. $18,200 gain.

C. $21,000 gain.

D. $38,000 gain.

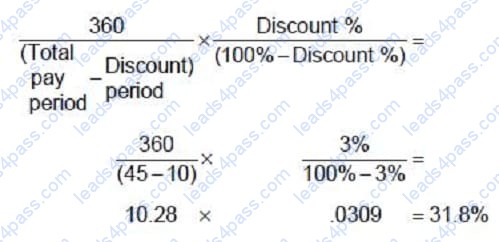

ABC Inc. purchases an item on credit with terms of 3/10, net 45. Based on a 360-day year, ABC's annual interest cost of foregoing the cash discount and making payment on the last day of the credit period is:

A. 24.00%

B. 30.86%

C. 31.81%

D. 37.11%

![]()

![]()

![]()

![]()

![]()

![]()

All rights are reserved by

leads4pass.com. Any changes, copy or trademarks abuse will be

regarded as infringement.

leads4pass.com will reserve the right to pursue accountability.

Copyright © 2004-

2026 leads4pass.com.